Let’s be honest. If budgeting feels like a chore, you’re probably not going to stick with it. Tracking every expense, categorizing every purchase, opening an app every single day — yeah, no thanks.

If you’ve ever thought “I want to manage my money better, just without all the effort,” this guide is for you. This is the lazy approach: a low-effort system for people who don’t want to think about money 24/7 but still want real results. (If your problem is more that budgeting feels miserable than that it feels like work, the mindset angle in how to start budgeting when you hate budgeting may fit better — this guide is purely about doing less.) It pairs naturally with fast, low-effort expense logging.

Quick Answer: How Do You Budget If You’re Lazy?

The lazy way to budget is to make the system run without you. Automate one savings transfer on payday, automate your bills, set a single monthly spending number, and do a five-minute weekly balance check. That’s the whole thing — no daily tracking, no categories. The trick isn’t more discipline; it’s removing the need for it.

Why Most Budgeting Advice Fails (Especially for Low-Effort People)

Spreadsheets. Apps. Categories. Daily tracking. Most traditional budgeting advice demands constant effort — and constant effort relies on constant motivation, which none of us have in unlimited supply.

Here’s what most financial guides won’t say out loud: if a system needs significant daily effort, most people won’t keep it up for long. That’s not laziness in the bad sense — willpower is finite, and a good system should make up for that instead of demanding you overcome it.

The easier your system is, the more likely you are to follow it. So instead of doing more, we do less — but smarter. Budgeting should feel like progress, not punishment, and low effort done consistently beats high effort done occasionally every time.

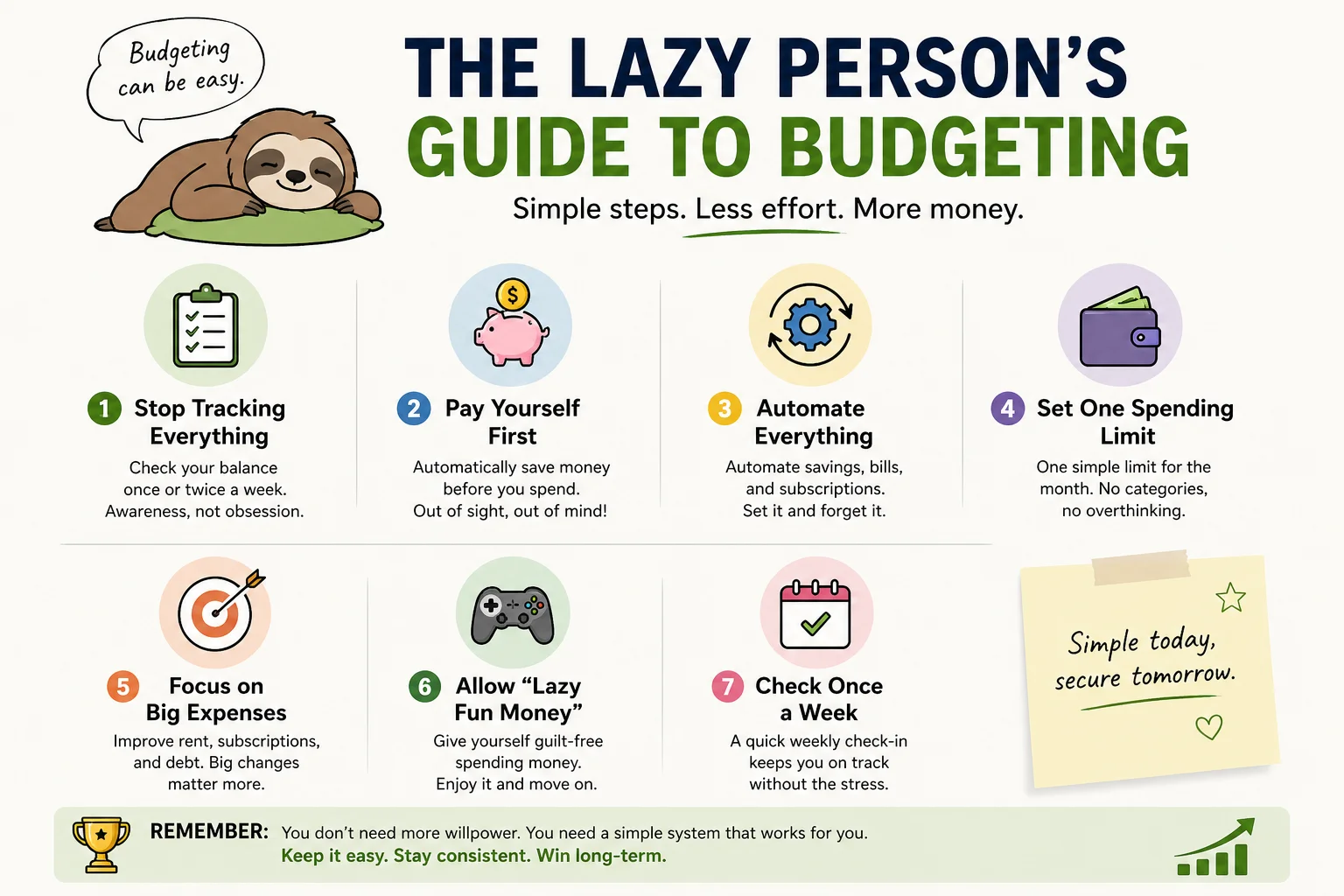

The 7 Hacks

You don’t need to log every coffee or keep a receipt for every transaction. What you need is general awareness, not forensic obsession. Check your total spending once or twice a week, notice whether it looks high or low against your usual pattern, and move on. The goal is awareness, not accounting.

This is both the laziest and the most effective personal finance move there is. On payday, automatically move a fixed amount to savings before you do anything else. Then spend whatever’s left without guilt or tracking. The saving happens automatically; the spending takes care of itself. No thinking required after setup.

Start with whatever feels painless — 5% of income, or a flat $50 (use whatever currency you budget in). The amount grows naturally once the habit sticks and you realize you don’t miss it. If watching the total climb helps, a savings goal or vault that fills as you go gives the automatic transfer something visible to feed.

If you have to remember it, you’ll occasionally forget it — so don’t rely on memory for anything important. Set up automatic transfers for savings, automatic payments for recurring bills, and automatic contributions for any investments. Once it’s automated, it runs without you, and your finances improve even in months you don’t think about money at all.

Automation doesn’t require discipline after setup — and setup takes about 20 minutes, once. That’s the most leverage you’ll ever get per minute spent on your money.

Forget budget categories. Forget sub-limits for dining, entertainment, and everything else. Just set one number: the total you can spend this month after savings and fixed bills are handled. One number, one rule. Spend below it and you’re winning. That level of simplicity is sustainable indefinitely.

The math takes ten seconds. Say you take home 2,000 a month: move 200 to savings, set aside 1,200 for fixed bills, and the remaining 600 is your one number — about 150 a week. That’s all you have to keep an eye on. If you’d rather split that leftover into a few simple buckets than ride one number, the beginner’s guide to budgeting walks through the fuller method step by step.

Cutting small purchases is exhausting and barely moves the needle. The highest-leverage review you can do is auditing your three largest monthly expenses: housing, transportation, and subscriptions. One reduction in any of these is worth more than eliminating dozens of small purchases. Spend your limited energy where the math actually matters.

Remove all spending on enjoyment and you’ll quit within two weeks — predictably, every time. Instead, set aside a fixed guilt-free amount each week for whatever you want: food trips, online shopping, entertainment. No tracking inside this bucket, no justification required. Spend it, enjoy it, move on. The boundary is the budget; what happens inside it is your business.

Daily financial review creates anxiety. Weekly review creates awareness. Pick one consistent day — Sunday morning works well — open your account, check your balance and spending against your monthly limit, note one thing, make one small adjustment if needed. The whole routine takes five minutes. That’s your entire active budgeting practice for the week.

Lazy Budgeting in Real Life

Here’s the full lazy system mapped against effort and outcome. Notice how the lowest-effort actions produce some of the highest-value results:

| Action | Effort Level | Result |

|---|---|---|

| Auto-save on payday | ● Very low (set once) | Consistent savings, no willpower needed |

| Automate bills & subscriptions | ● Very low (set once) | Zero missed payments, no mental overhead |

| Set one monthly spending limit | ● Low (5 min/month) | Clear spending boundary without category tracking |

| Weekly 5-min balance check | ● Low (weekly) | Awareness without burnout |

| Fun money allowance | ● Zero tracking | Sustainable long-term — you don’t feel restricted |

| Daily detailed tracking | ● High (daily) | Often abandoned within a few weeks |

A daily action in Hunter Vault takes under two minutes — log one expense, check one balance, confirm one savings transfer — and you get XP, a streak, and rank progress for doing that minimum viable habit. That tiny reward loop is what keeps a low-effort system going long-term, which is the hardest part. It won’t do the saving for you, but it makes showing up easy. Try Hunter Vault free →

The 20-Minute Automation Setup (The Part Everyone Skips)

Most “automate it” advice stops at the word automate. Here’s the actual order of operations — do it once and the lazy system basically runs itself.

- Automate the savings transfer first, scheduled for payday itself (or the next morning, if your pay lands at midnight). Saving before anything else leaves the house means it never competes with spending.

- Schedule bill payments for 1–2 days after payday, not on the same day. That small buffer stops a bill from hitting before your paycheck has fully cleared and triggering an overdraft.

- Leave the rest in your spending account — that’s your “one number” from Hack 4. No sub-accounts needed.

- Set one calendar reminder for your five-minute Sunday check, so the only manual task you have is impossible to forget.

That’s the whole stack: money out to savings, bills handled, the remainder visible, one weekly nudge. Twenty minutes of setup buys you months of not thinking about it.

Savings transfer on payday, bills a day or two later, spending money is whatever’s left. Get that sequence right and overdrafts and “I forgot to save this month” mostly disappear on their own.

Common Mistakes Lazy Budgeters Make

Even with a minimal system, a few patterns reliably derail people:

- Trying to implement everything at once — pick one or two hacks first, then layer in the rest over a few weeks

- Aiming for perfection immediately — a slightly messy low-effort system beats a perfect one you abandon on day eight

- Choosing complicated apps — the tool should take less effort than the habit it supports, not more (more on why budgeting apps get abandoned)

- Quitting after one bad week — overspending once is data, not a reason to scrap the approach

- Skipping the automation setup — those five minutes are the single highest-return use of time in this entire guide

Adding more rules, categories, or tracking to “fix” a struggling budget almost always makes it worse. If the system isn’t working, simplify it further — don’t complicate it.

Frequently Asked Questions

Can budgeting really be this simple?

Yes — and simpler systems tend to win over the long run because they’re easier to maintain. A basic system followed for twelve months beats a detailed one abandoned after two weeks. Simplicity isn’t a compromise here; it’s the strategy.

What if I overspend one week?

Adjust slightly the following week and move on. One overspent period doesn’t mean restarting your system or feeling guilty. This approach is built to be resilient to imperfect months — you rebalance rather than restart.

Do I need a budgeting app?

No. The foundation is automation — a scheduled savings transfer and automatic bill payments that run without any app involvement. Beyond that, a weekly balance check takes five minutes and works fine with your bank’s own app or even a notebook.

How much should I save?

Whatever is painless right now. Start at 5%, or a flat $50 a month (or the equivalent in your currency). The habit of saving automatically matters far more than the amount. Nudge it up every few months as your income grows or expenses drop.

Is this better than traditional budgeting?

For long-term consistency, yes. Detailed, daily-tracking systems look better on paper, but most people abandon them. Consistency is the variable that determines real-world outcomes, and a lazy system you keep for years beats a perfect one you use for weeks.

What if I forget to check my budget?

That’s exactly why automation sits at the foundation. If you skip a weekly check-in, your savings transfer still happened, your bills still got paid, and your finances still improved. The system runs without your active participation — which is the whole point.

Conclusion: Lazy Doesn’t Mean Bad With Money

People who resist traditional budgeting aren’t bad with money. They’re rejecting systems that demand more ongoing effort than any human reliably provides. That’s a reasonable response to bad system design, not a character flaw.

The lazy approach works because it’s built around how people actually behave: inconsistently, imperfectly, with limited daily motivation. Automation handles the critical behaviors. The weekly check-in handles awareness. The fun-money allowance handles sustainability.

- Set up one auto-savings transfer this week — start there

- Automate your recurring bills so they never need a decision

- Set one monthly spending number — not twenty categories

- Give yourself guilt-free fun money every week

- Check your balance for five minutes every Sunday — that’s your entire active practice

- Optional: let Hunter Vault handle the streak and the weekly nudge so the habit sticks

Do the 20 minutes of setup once, then let the system carry the rest. Months from now, the lazy version will still be quietly running — which is more than most elaborate budgets can say.