The first time I heard about the 50/30/20 rule, I thought: nice, simple, clean — this should be easy.

It wasn’t. I tried splitting my money exactly like the rule said, and within a month, everything was off. My “needs” were already over 50% before I even got to rent. My “wants” didn’t magically shrink because a framework said they should. And my savings? Basically vibes.

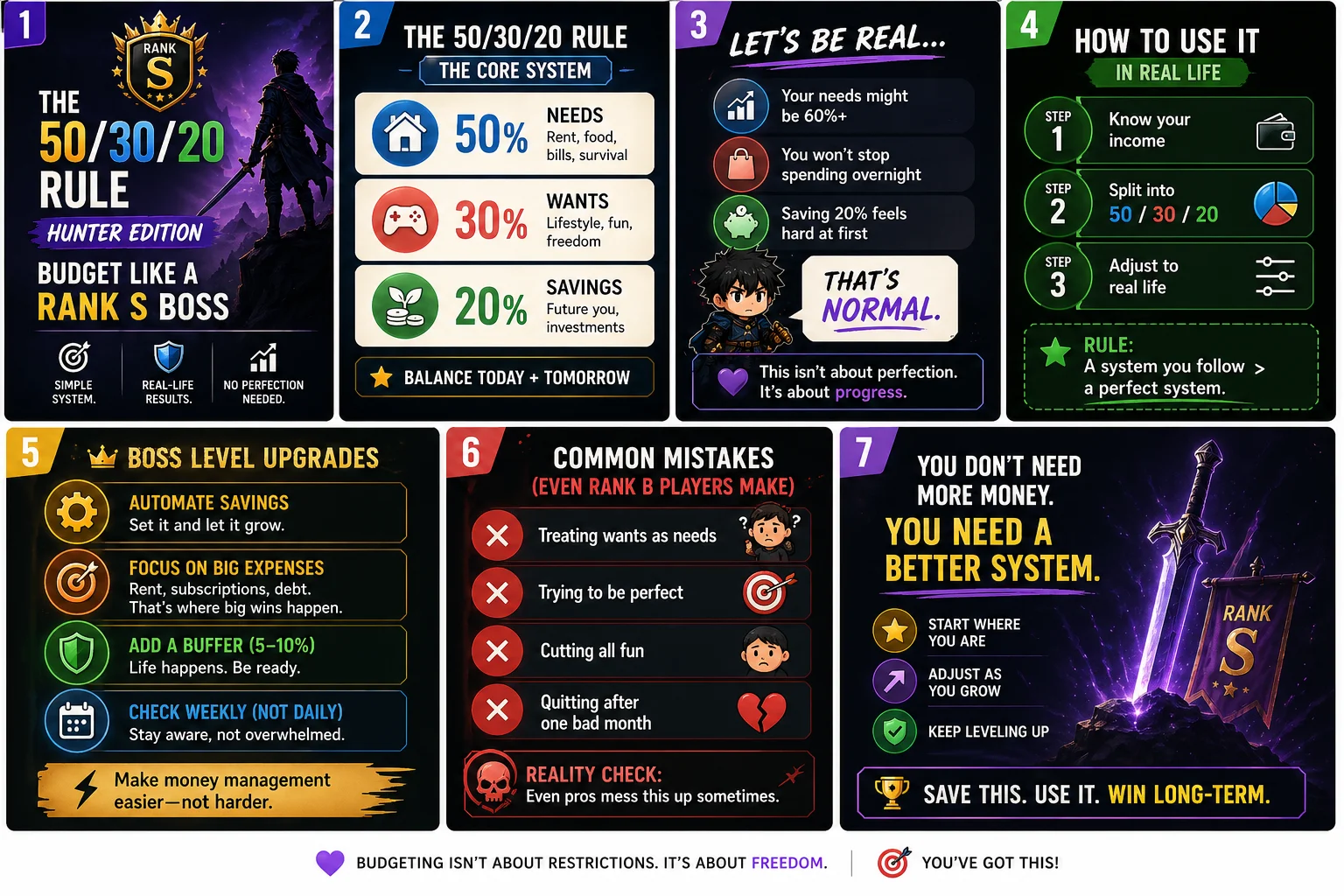

That’s when it clicked: the rule isn’t broken. The way most people are taught to apply it is. So instead of forcing perfect percentages, I started treating my budget like a resource management system — which is exactly the mindset shift this guide is about. Hunter Vault’s budget planner has the 50/30/20 split built in if you want a head start.

What Is the 50/30/20 Rule?

Here’s the version without the textbook explanation:

On paper, that balance looks clean. In practice, most people’s needs alone blow past 50% before they even think about wants — and that’s exactly why we need to approach this differently.

Hunter Edition Mindset: Allocate, Don’t Restrict

The standard framing of the 50/30/20 rule is about restriction: keep needs under this, keep wants under that, force savings up to here. That framing is why it fails for most people.

The Hunter Edition reframe is simple: you’re not following rules — you’re allocating resources. Money is a resource. You decide where it goes. Every allocation is a choice you made, not a limit someone imposed on you.

Instead of “I need to follow this rule perfectly,” think: “I’m managing resources like a strategist.”

That shift changes everything. You stop feeling restricted. You start making intentional decisions. And — critically — you actually stick with it past week two.

Why Most People Struggle With This Rule

Here’s what most 50/30/20 guides skip.

Your needs might already be over 50%

Rent alone consumes half the income of a huge portion of working adults. When someone living in a city reads “keep needs under 50%,” they’re often already at 55–65% before adding food or transport. This isn’t a budgeting failure — it’s just the reality of housing costs. The rule was created when cost-of-living ratios looked very different.

Your wants don’t disappear on command

Telling yourself you’ll cut all discretionary spending lasts about two weeks. Then you snap, overspend on one night out, feel guilty, and quit the whole system. This is the pattern, not the exception. Wants aren’t weakness — they’re a necessary part of a sustainable budget.

20% savings feels impossible from zero

If you’re starting from scratch — no emergency fund, some debt, irregular income — being told to save 20% immediately is discouraging. It creates an all-or-nothing framing that guarantees failure for people who most need the habit.

The 50/30/20 rule is most useful as a target to work toward over months — not a standard to meet on day one. Treat it as a compass, not a scorecard.

If you haven’t set up a budget before, the beginner’s guide to budgeting walks through the full setup step by step before diving into methods like this one.

The Real Way to Apply Each Bucket

Needs are non-negotiables: rent, utilities, groceries, transport, minimum debt payments, health insurance. These come first — always.

If your needs exceed 50%, that’s normal. Don’t panic and don’t quit. Instead, ask two questions: What’s my single biggest expense? Can I reduce it over the next 6–12 months? That’s the only action item here — identify the lever, don’t try to cut everything at once.

Wants are everything that makes life enjoyable: dining out, entertainment, hobbies, clothes, coffee, subscriptions you actually use. This category isn’t a luxury — it’s load-bearing infrastructure for your budget.

The approach: set a realistic limit, spend it without guilt, then stop when it’s gone. No detailed tracking inside this bucket. A weekly fun budget that you can spend however you want is more sustainable than twenty sub-categories you obsessively monitor.

The biggest mistake beginners make here is aiming for 20% immediately. Start with 5%, automate it, and build the habit. The percentage matters far less than the consistency. A ₱500/month savings habit you maintain for three years is worth more than a 20% savings rate that lasts six weeks.

Priority order for this bucket: emergency fund first (3–6 months of expenses), then debt payoff, then investing. Don’t invest while carrying high-interest debt — the math doesn’t work in your favor.

How to Actually Make This System Work

Three changes make the difference between a rule you read about and a system you actually use.

Granular daily tracking is exhausting and unsustainable for most people. Instead, track at the bucket level. Did you stay roughly within your Needs allocation? Did your Wants spending feel reasonable? Is your savings transfer confirmed? That’s enough information to run this system effectively. (If granular tracking has always been your sticking point, the lazy person’s guide to budgeting leans all the way into that.)

Set a recurring transfer to your savings account on the same day your paycheck arrives. Even ₱500 or 5% — whatever your starting number is. This is the single highest-leverage change you can make because it removes the savings decision from your daily life entirely. The money is gone before spending temptation enters the picture.

One five-minute check-in per week keeps you aware without the burnout of daily monitoring. Review total spending against each bucket, note anything surprising, adjust one thing if needed. That’s the entire weekly practice. Daily financial review creates anxiety — weekly review creates awareness.

Boss-Level Upgrades

Focus on the big wins, not the small ones

Cutting your daily coffee saves a few thousand pesos a year. Negotiating your rent, canceling two unused subscriptions, or refinancing high-interest debt can save ten times that. Audit your three largest expenses before touching anything else — that’s where the real game is.

Add a buffer category

Build a 5–10% buffer into your Needs bucket for irregular expenses — a car repair, a doctor’s visit, a birthday you forgot. A budget that has no room for surprise will break every time life is surprising, which is constantly. The buffer is what separates a brittle plan from a durable one.

Hunter Vault’s Quest Log aligns directly with the three buckets — Needs quests, Wants limits, and Savings goals each generate XP when you hit them. Instead of red warning bars when you overspend, you get progress toward rank-up. That positive reinforcement loop is what keeps the habit alive past week two. See how it works →

Accept imperfect months — plan for them

Even with a solid system, some months will run over budget. A family event, an unexpected bill, a particularly good sale. The goal isn’t a perfect record — it’s a consistent long-term trend. One overspent month inside an otherwise solid three months still represents real progress.

Common Mistakes (Most People Make All of These)

- Trying to hit perfect percentages immediately — the rule is a target, not a day-one requirement

- Cutting all discretionary spending — this is how people quit budgeting entirely within two weeks

- Tracking every single transaction — obsessive tracking creates friction that kills the habit

- Giving up after one bad month — one overspend doesn’t erase progress; abandoning the system does

- Comparing your split to someone else’s — cost of living, income, and life stage vary too much for meaningful comparison

Treating a bad month as proof that you “can’t budget.” One rough month is data — not a verdict. Adjust and continue.

A Realistic Example (₱30,000/month)

This isn’t a textbook-perfect split. It’s what it actually looks like when rent is high and you’re still building your savings habit:

| Bucket | Target % | Target Amount | Real-Life Amount |

|---|---|---|---|

| Needs | 50% | ₱15,000 | ₱18,000 (rent is high) |

| Wants | 30% | ₱9,000 | ₱7,000 |

| Savings | 20% | ₱6,000 | ₱5,000 |

The split isn’t perfect — and it still works. Savings are happening. Wants have a limit. Needs are covered. That’s the whole point of the framework: directional clarity, not numerical perfection.

Frequently Asked Questions

Do I need to follow the 50/30/20 rule exactly?

No. It’s a guideline, not a contract. The percentages are targets to work toward over time — not a standard you need to meet on day one. Adjust the split to reflect your actual income and cost of living, and revisit it every few months as your situation changes.

What if I can’t save 20% yet?

Start with whatever is realistic — 5%, a flat ₱500, even ₱200. The habit of saving something consistently is far more valuable than hitting a specific percentage. The amount grows naturally once the behavior is established.

Can I still enjoy life while following this rule?

You should. The Wants bucket exists precisely so you can enjoy your money without guilt. Cutting all fun spending leads to binge spending and abandonment — predictably and quickly. Budget for enjoyment intentionally rather than trying to eliminate it.

What if my expenses are too high?

Focus on your single largest expense first. For most people that’s rent or housing. Even a 10% reduction there is worth more than eliminating a dozen small purchases. Don’t stress the small stuff until the big stuff is addressed.

How long until this feels normal?

Most people find a simplified version of this system feels comfortable within three to four weeks of consistent use. Keep the system low-maintenance early on — the habit has to form before you refine the percentages.

Is this better than a strict line-item budget?

For most people in most situations, yes. Strict budgets require significant ongoing effort and collapse under real-life conditions. The 50/30/20 framework provides enough structure to guide decisions without demanding daily perfection.

Final Thoughts: This Isn’t About Perfection

The 50/30/20 rule isn’t about hitting exact numbers. It never was. It’s a framework for understanding where your money goes, building better habits around it, and creating a system you can actually live with — not just one that looks clean on a spreadsheet.

The Hunter Edition mindset is simple: you’re not following a rule. You’re managing a resource. Every peso you allocate intentionally is a decision you made — and that shift in ownership changes everything about how sustainable the habit becomes.

- Start with the three buckets — don’t over-complicate it with sub-categories

- Automate your savings transfer before spending anything else

- Accept that your Needs might exceed 50% for now — work the big levers over time

- Protect your Wants budget — a budget without enjoyment is a budget you’ll quit

- Review weekly, not daily, and adjust one thing at a time

The best budget is the one you don’t quit. Start wherever you are, keep it simple, and let the habit compound over time.